Download the report by clicking the link at the top right or bottom right of the page.

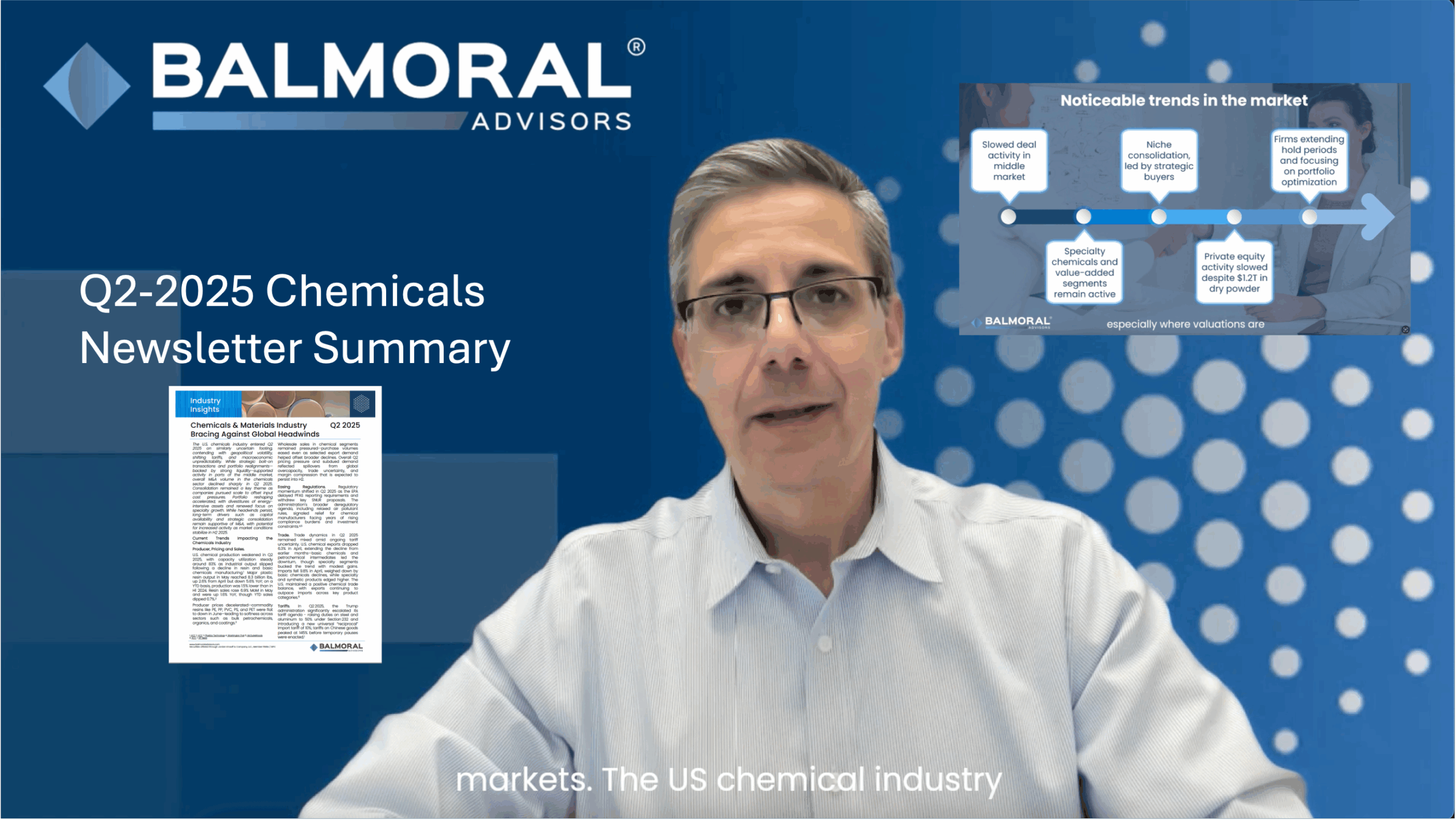

The U.S. chemicals industry entered Q2 2025 on similarly uncertain footing, contending with geopolitical volatility, shifting tariffs, and macroeconomic unpredictability. While strategic bolt-on transactions and portfolio realignments—backed by strong liquidity—supported activity in parts of the middle market, overall M&A volume in the chemicals sector declined sharply in Q2 2025. Consolidation remained a key theme as companies pursued scale to offset input cost pressures. Portfolio reshaping accelerated, with divestitures of energy-intensive assets and renewed focus on specialty growth. While headwinds persist, long-term drivers such as capital availability and strategic consolidation remain supportive of M&A, with potential for increased activity as market conditions stabilize in H2 2025.